Are you approaching Medicare eligibility and wondering about the financial implications? One crucial aspect to understand is the cost of Medicare Plan B, which covers medically necessary services like doctor visits and outpatient care. Navigating the complexities of Medicare can feel overwhelming, but having a clear grasp of Plan B expenses is essential for informed decision-making and effective budget planning.

Many individuals ask, “What is the price tag associated with Medicare Plan B?” The truth is, there isn’t one fixed answer. Medicare Plan B premiums are subject to change annually, and several factors influence the final amount you'll pay. These include your income, when you enroll, and whether you’re still working. Grasping these variables is crucial for accurately anticipating your healthcare expenses.

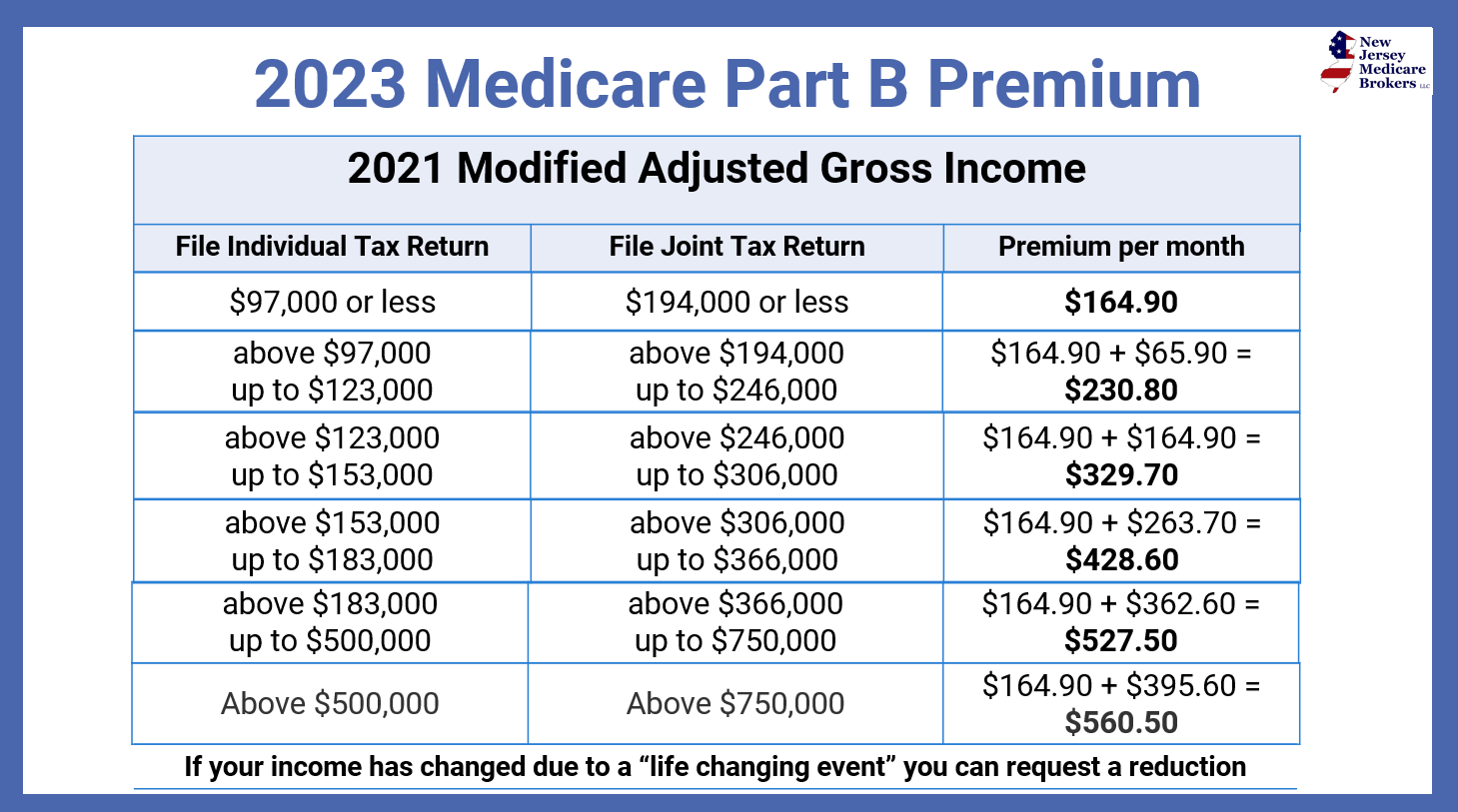

Historically, Medicare Plan B premiums have been tied to income levels. Higher earners typically pay more for their coverage. This income-related adjustment ensures that those with greater financial resources contribute a larger share to the Medicare system. However, understanding the specific income thresholds and corresponding premium amounts is vital for accurate budgeting. This information is typically updated annually by the Centers for Medicare & Medicaid Services (CMS).

Medicare Plan B is a critical component of the overall Medicare program, designed to ensure access to essential medical services. It plays a vital role in protecting beneficiaries from potentially catastrophic healthcare costs. Without Plan B coverage, many individuals would face significant financial burdens when seeking necessary medical care. Therefore, understanding the cost of Plan B and factoring it into your budget is essential for financial well-being in retirement.

One of the most common questions surrounding Medicare Plan B costs is, "How is the premium calculated?" The standard premium is a base amount set by CMS each year. However, individuals with higher incomes, as determined by their modified adjusted gross income (MAGI) from two years prior, pay a higher premium, known as an Income Related Monthly Adjustment Amount (IRMAA). It's crucial to understand how IRMAA can affect your out-of-pocket expenses. This information is readily available from the Social Security Administration and CMS.

In addition to the monthly premium, Medicare Plan B also has an annual deductible. This is the amount you must pay out-of-pocket for covered services before Medicare begins to pay its share. Understanding both the premium and deductible is crucial for accurately estimating your healthcare costs.

Beyond premiums and deductibles, understanding potential cost-sharing, such as coinsurance and copayments for specific services, is vital for comprehensive budgeting. Coinsurance is the percentage of the cost of a service you’re responsible for after meeting your deductible. Copayments are fixed dollar amounts you pay for certain services. Having a clear picture of these costs allows for better financial planning.

Benefits of Understanding Medicare Plan B Costs:

1. Accurate Budgeting: Knowing the cost of Plan B allows you to create a realistic budget for healthcare expenses in retirement.

2. Informed Decision-Making: Understanding Plan B costs helps you make informed choices about your overall Medicare coverage and supplemental insurance options.

3. Avoid Financial Surprises: By anticipating Plan B expenses, you can avoid unexpected financial burdens and maintain financial stability during retirement.

Advantages and Disadvantages of Medicare Plan B

| Advantages | Disadvantages |

|---|---|

| Covers a wide range of medically necessary services | Monthly premiums and annual deductible |

| Provides financial protection against high healthcare costs | Cost sharing for some services (coinsurance/copayments) |

Frequently Asked Questions about Medicare Plan B Costs:

1. How much does Medicare Plan B cost? The cost varies depending on your income and other factors.

2. What does Medicare Plan B cover? It covers medically necessary services like doctor visits and outpatient care.

3. How is the Plan B premium calculated? It's based on a standard premium with adjustments for higher earners.

4. What is the Medicare Plan B deductible? It's the amount you pay out-of-pocket before Medicare starts paying.

5. How can I find out my specific Plan B premium? Contact Social Security or visit the Medicare website.

6. What is IRMAA? It's the Income Related Monthly Adjustment Amount for higher earners.

7. Does Plan B cover prescription drugs? No, prescription drug coverage is provided by Part D plans.

8. Can I change my Plan B coverage? You can generally make changes during certain enrollment periods.

Tips and Tricks: Utilize online resources like the Medicare.gov website and the Social Security Administration's website to access up-to-date information on Plan B premiums, deductibles, and coverage details. Consult with a Medicare advisor for personalized guidance on navigating the complexities of Medicare Plan B and optimizing your healthcare coverage.

Understanding the cost of Medicare Plan B is paramount for anyone approaching Medicare eligibility. By familiarizing yourself with the factors influencing premiums, deductibles, and cost-sharing, you can effectively plan for your healthcare expenses in retirement. This knowledge empowers you to make informed decisions about your coverage, avoid unexpected financial burdens, and maintain your financial well-being. Take proactive steps to research your options, compare plans, and seek guidance from reputable sources like Medicare.gov to make the most of your Medicare benefits and ensure a secure financial future. Don't wait, start planning today to ensure you're prepared for the financial aspects of Medicare Plan B. It's crucial for your peace of mind and long-term financial health.

Obsessed with sherwin williams green stain youre not alone

Snag that google logo svg download mania

Pastel butterflies a whimsical wonder