Navigating the Medicare landscape can feel like traversing a digital labyrinth. You've got your Part A, your Part B, and then... the alphabet soup continues. One crucial piece of this puzzle is Medicare Plan E, a supplemental insurance option designed to help manage out-of-pocket healthcare expenses. But what exactly does it cover? Is it the right choice for you? Let's decode the complexities of Medicare Plan E benefits and empower you to make informed decisions about your healthcare coverage.

Medicare Plan E is designed to help fill the gaps in Original Medicare (Parts A and B) coverage. Imagine it as a safety net, catching those costs that might otherwise hit your wallet hard. These costs include hospital deductibles, coinsurance, and copayments. For many on a fixed income, these expenses can be a significant burden. Understanding how Plan E coverage functions is essential for effective healthcare budgeting and financial well-being.

Historically, Plan E was the most comprehensive of the Medicare Supplement plans, also known as Medigap. Introduced as part of the standardized Medigap plans in 1990, it provided coverage for virtually all out-of-pocket costs not covered by Original Medicare. However, with the introduction of Medicare Part D prescription drug coverage in 2006, Plan E no longer covers the Part B deductible. This change addressed rising premium costs and streamlined the Medigap options.

The primary purpose of a Medicare Supplement Plan E is to provide predictable healthcare expenses. While Medicare covers a significant portion of medical costs, it doesn't cover everything. This is where Plan E steps in, offering financial peace of mind. Understanding the scope of these supplemental benefits is key to managing your healthcare budget, particularly during retirement.

A key issue surrounding Medicare Plan E benefits is the understanding of its coverage in comparison to other Medigap options. Plan E offers a balance between comprehensive coverage and affordability, but it's essential to compare it to other plans (like Plan G or Plan N) to determine the optimal fit for your individual healthcare needs and financial situation. This requires a careful assessment of potential medical expenses, risk tolerance, and budgetary constraints.

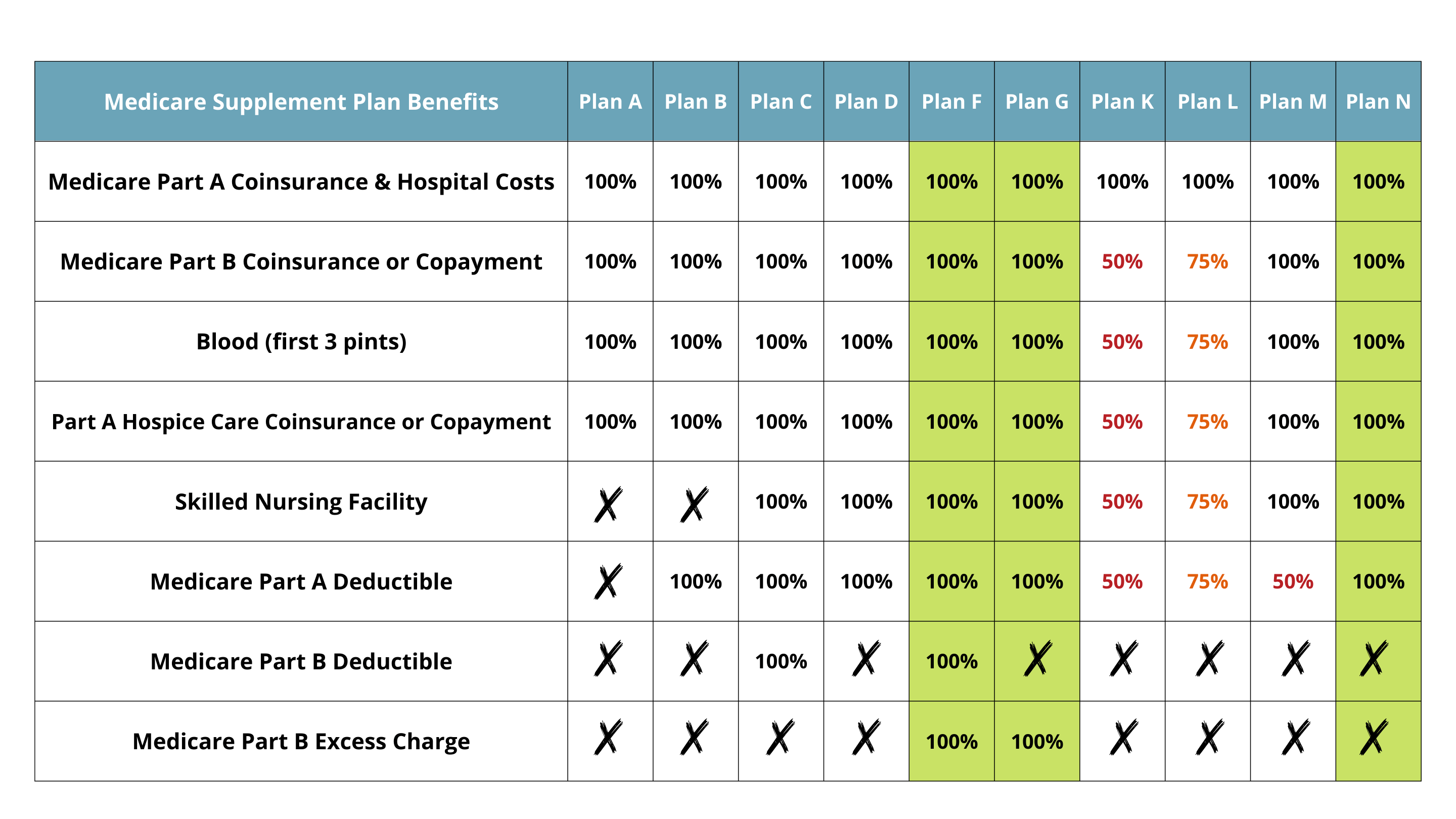

Medicare Plan E primarily covers hospital coinsurance, medical coinsurance, blood transfusions (after the first 3 pints), and hospice care coinsurance. For example, if you have a hospital stay, Medicare Plan E would pick up the coinsurance costs you would otherwise be responsible for. It does not cover the Part B deductible, skilled nursing facility care coinsurance, or foreign travel emergency expenses.

One benefit of Plan E is its predictability in terms of cost-sharing. Knowing precisely what your out-of-pocket expenses will be can significantly reduce financial stress. Another benefit is the simplified healthcare billing process. With Plan E, you have fewer bills to manage, making healthcare administration less complicated.

Advantages and Disadvantages of Medicare Plan E

| Advantages | Disadvantages |

|---|---|

| Predictable out-of-pocket expenses | Doesn't cover Part B deductible |

| Simplified billing process | May not be the most comprehensive option |

Frequently Asked Questions about Medicare Plan E

1. What does Medicare Plan E cover? Hospital coinsurance, medical coinsurance, blood transfusions (after 3 pints), and hospice care coinsurance.

2. Does Plan E cover the Part B deductible? No.

Choosing the right Medigap plan is crucial. Thoroughly compare available options to determine what aligns with your needs. Consulting with a licensed insurance broker specializing in Medicare can provide valuable guidance.

In conclusion, navigating the complexities of Medicare supplemental insurance requires careful consideration and a clear understanding of your healthcare needs. Medicare Plan E offers a valuable option for managing out-of-pocket costs, particularly for those seeking predictable expenses and a streamlined billing process. While it might not be the most comprehensive Medigap plan available, its balance of coverage and affordability makes it a compelling choice for many. By thoroughly researching your options, comparing plans, and consulting with a qualified insurance professional, you can confidently choose the best supplemental coverage to secure your healthcare future.

The intriguing narrative of william afton and elizabeth in five nights at freddys

Unlocking the power of benjamin moore paint hues

Crimson craze decoding the red aesthetic laptop wallpaper obsession